Atradius Atrium

Sie erhalten direkten Zugriff auf Ihre Vertragsinformationen, Tools zur Beantragung von Kreditlimits und Einblicke.

Österreich

Österreich

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Dänemark

Deutschland

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Österreich

Norwegen

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

UK companies continue to use trade credit cautiously as they navigate a fragile economic landscape marked by high finance costs, uneven demand, and persistent cost pressures. Around 68% of B2B sales are made on credit, an increase during recent months, and now 16 percentage points above the Western European average. This gap reflects a deliberate balancing act by UK firms, with the expansion of trade credit being a measured trade-off between supporting growth and managing risk.

Trade credit decisions are shaped by the current volatile economic and trading environment amid severe geopolitical uncertainty and softened global demand. Despite an easing of inflation, liquidity conditions are tight and cost pressures remain an issue. Business failures continue to be high in the UK, particularly among smaller firms in the construction, trade, and consumer-facing sectors. This means the risk associated with customer failure has become more acute. In this challenging environment most UK companies continue to anchor payment terms at about 30 days. However, they are far less likely than those in Western Europe to move from short to longer terms, with extensions relatively uncommon. Trade credit in the UK thus remains closely managed, with firms seeking to preserve control rather than absorb additional structural risk.

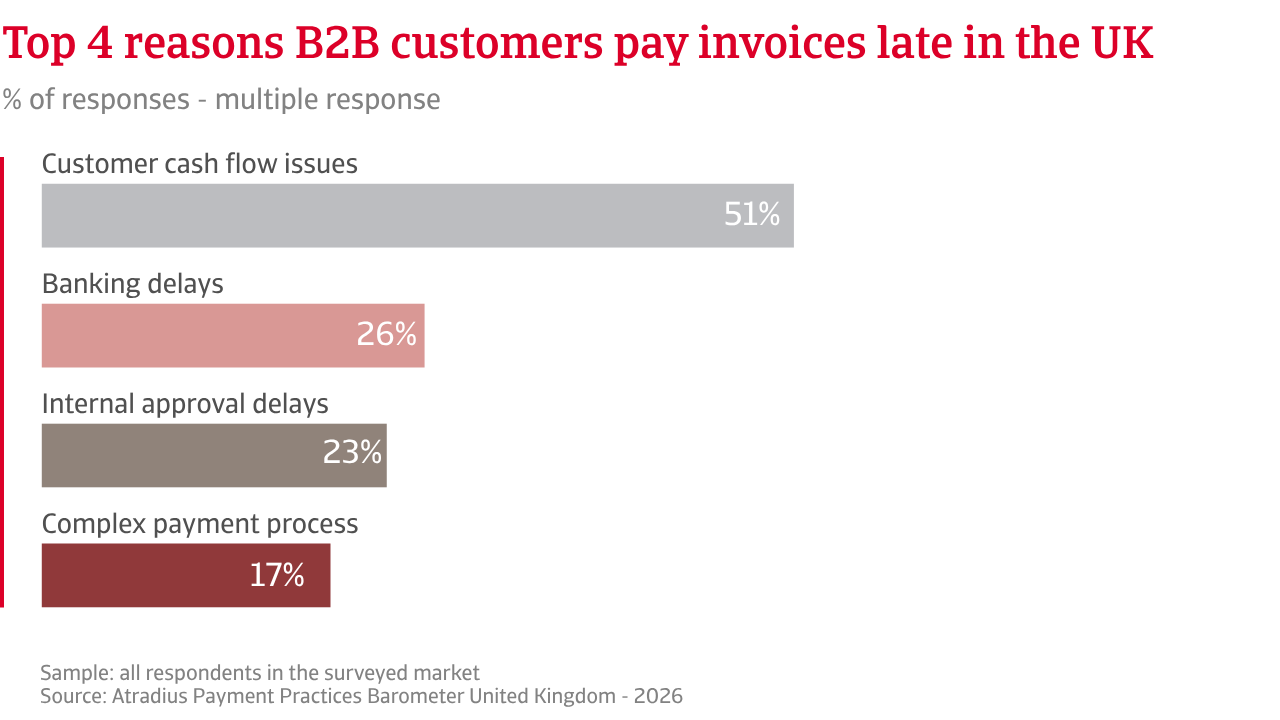

Late payments remain a problem in the UK, although less severe than across Western Europe. Around two thirds of UK businesses report delayed payments from B2B customers, compared with more than three quarters across the region. These delays affect about 25% of invoiced B2B turnover in the UK, slightly below the Western European benchmark. UK firms tend to collect payments faster than in Western Europe, keeping average Days Sales Outstanding lower. Another difference, however, is that when payments fall behind in the UK, they are more likely to drift into long-term overdue. UK companies report bad debt losses of up to 2% of B2B invoices, largely driven by customer insolvency. Western Europe has slower collection at mid-range overdue stages, but fewer very long delays. The result is a different risk profile rather than a lower one.

The impact of payment behaviour on working capital also diverges. Our survey shows Western European companies are far more likely to scale back investment in growth or innovation as a direct response to late payment. Reliance on external financing follows a similar pattern, with significantly more firms in Western Europe reporting increased dependence on third party funding. While working capital stress is present among UK companies, it remains less pervasive.

UK firms continue to rely heavily on active credit management to control payment risk, including close monitoring of customers, digital reminders, and early payment incentives. Credit insurance plays a role, but is used less extensively than in Western Europe, where companies tend to combine internal controls with broader risk transfer.

Most UK companies continue to anchor payment terms at about 30 days. They are far less likely than those in Western Europe to move from short to longer terms, with extensions relatively uncommon.

UK businesses approach the coming months with little momentum and face rising pressure. The Middle East conflict is adding an energy shock to an already fragile economy, pushing inflation higher and forcing the Bank of England to stay cautious. With rate cuts delayed into late 2026 or early 2027, businesses face higher costs for longer. There are also limited expectations of change in B2B payment behaviour, which reflects ongoing restraint rather than renewed confidence. While most UK firms do not see any meaningful change in B2B payment behaviour, views on any potential change are evenly split between optimism and caution. This contrasts with Western Europe, where downside risks dominate sentiment, reflecting weaker confidence in the global economic and trade landscape.

Survey findings show that UK businesses focus on concerns closer to home, with domestic cost pressures and finance conditions shaping their expectations. The domestic macroeconomic backdrop remains challenging. Growth has stayed modest, demand is fragile, and cost pressures are ongoing. Inflation is anticipated to stay elevated, operating costs are higher, and interest rates continue to weigh heavily, all of which keeps working capital stretched. For many firms this has translated into tighter cash buffers at a time when payment risk remains stubbornly high.

This pressure is underlined by an expectation among companies in the UK that current high levels of insolvencies will persist, at least in the short term. The construction and wholesale trade sectors account for the highest share of failures as they face a combination of soft demand, rising input costs, and structurally thin margins. A minority predicts a rise in insolvencies, while the remaining respondents do not have a clear-cut opinion. There is a similar lack of optimism about the prospects for profitability, with UK businesses expressing reduced confidence in their ability to protect margins. Concerns around erosion are markedly stronger than in Western Europe. With less financial headroom, companies have limited capacity to absorb late or missed payments. Western European firms appear better positioned, despite similarly modest growth prospects.

Companies in both the UK and Western European identify economic conditions as the primary threat to B2B payments. UK firms focus more strongly on cost inflation, financing strain, and sector specific downturns. This aligns with insolvency concentrations in construction and wholesale trade, highlighting internal market stress. Western Europe assigns greater weight to geopolitical and market related risks. Cross border exposure, policy uncertainty, and the global trade landscape feature more prominently. Payment risk across the region stems less from domestic fragility and more from external shocks.

For a full overview of the 2026 survey results for the United Kingdom and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Rückruf anfragen

Rechtlicher Hinweis