Atradius Atrium

Sie erhalten direkten Zugriff auf Ihre Vertragsinformationen, Tools zur Beantragung von Kreditlimits und Einblicke.

Österreich

Österreich

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Dänemark

Deutschland

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Österreich

Norwegen

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

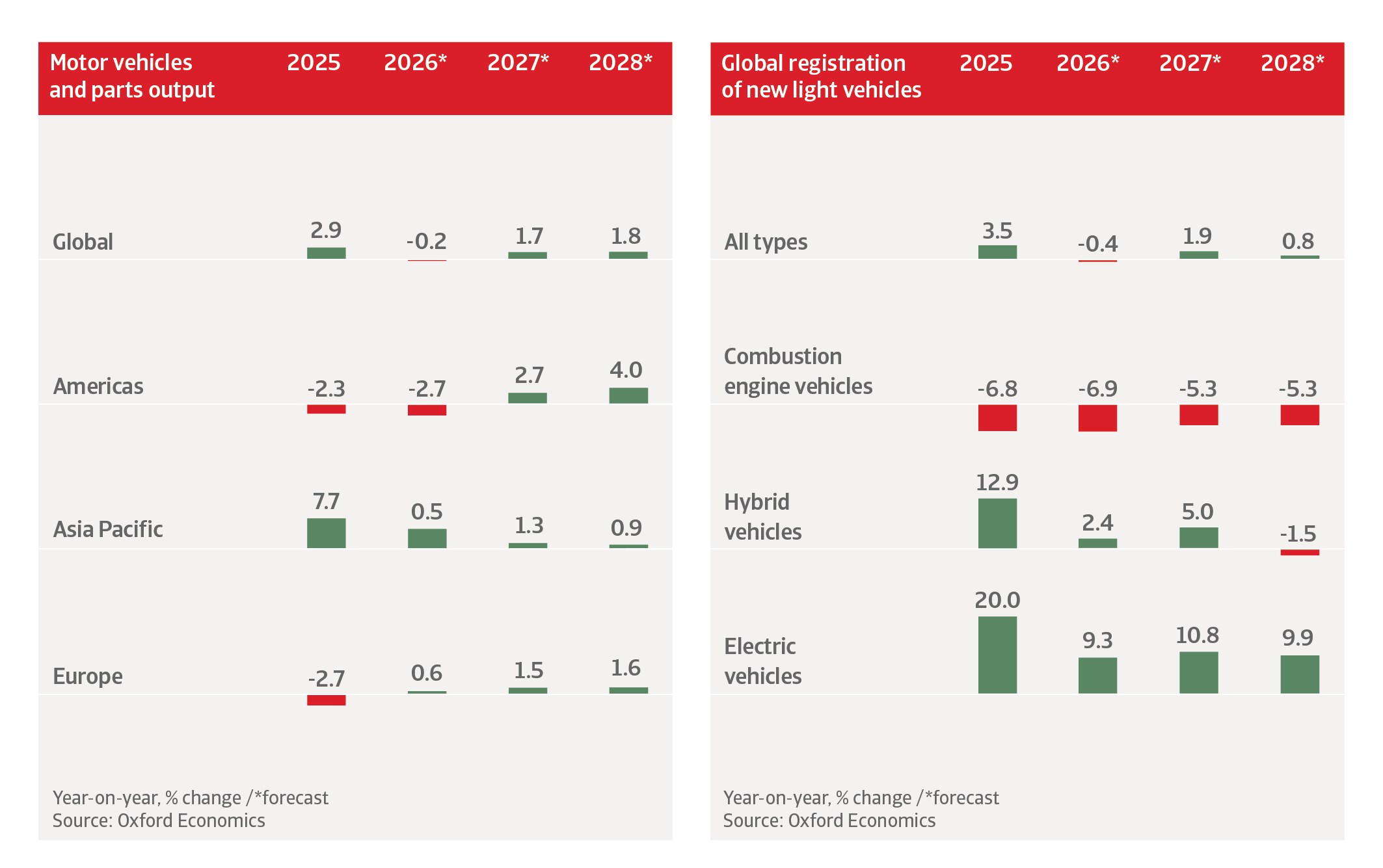

We expect global production of motor vehicles and parts to decrease by 0.2% in 2026, after a 2.9% increase last year. Trade protectionism, an uneven electric vehicle (EV) transition, and subdued consumer confidence are weighing on production across most major markets. Regionally, the performance is very different. China continues to drive growth while developed-market producers, particularly in Europe, face simultaneous headwinds from demand weakness, cost pressures, and structural overcapacity. Across all regions, the war in the Gulf from late February to mid-June has led to sharply increased energy prices and weakened consumer confidence. Although oil prices have started to decline, the past hit to consumers’ real disposable incomes is likely to weigh on discretionary goods spending, which includes new vehicles. In 2027, we expect global automotive production to grow by 1.7%, mainly due to a recovery in the Americas, particularly the US.

The modern automotive industry operates in a globally competitive marketplace. Production has become increasingly globalised, with original equipment manufacturers (OEMs) relying on a complex network of global suppliers. The industry is highly susceptible to downside risks like rising geopolitical tensions, the institutionalisation of global auto tariffs and deglobalisation trends, leading to supply chain disruptions. One example of this is when China announced its intention to impose very tight export controls on rare earths in October 2025, following a Sino-US trade spat. The decision was soon softened, but nevertheless exposed the vulnerability of Western automotive producers due to high dependency on critical minerals. Restrictions on rare earths would have affected the production of electric vehicles (EVs) and other electrical systems, including electric motors, sensors, power steering, and regenerative braking systems. OEMs would have faced significant exposure to risks from a potential supply chain bottleneck. Breaking China’s commanding position in the rare earths sector will remain a long-term challenge, with Beijing expected to retain its strategic leverage over these critical minerals.

Currently, electric vehicle sales are facing headwinds in the US, as the government has rolled back EV tax credits. In Europe’s main markets, demand for EVs is growing only slowly. In China, the EV transition maintains strong momentum, but both the US and the EU have imposed punitive tariffs on Chinese EV imports. That said, we expect global hybrid and EV sales to account for 59% of global light vehicle sales by 2030, up from 10% in 2020.

US automotive output is forecast to decrease by 2.8% in 2026 after a 1.3% contraction last year, as ongoing trade uncertainty and tariff-related disruptions weigh on both production and demand. Last year, levies on imported vehicles and parts squeezed the operating margins of OEMs as they absorbed higher input costs, although many also passed on more of the tariff burden to consumers. The price increases weigh on demand for both imported and domestically produced vehicles. Although petrol prices have softened, the past hit to real disposable income growth will negatively affect spending. This, together with an expiration of the EV tax credit, tariff pass-through, and payback for frontloaded purchases in 2025, will likely slow the pace of vehicle sales this year, and we expect passenger car sales to decrease by 1%.

The US automotive sector depends on regionally and globally integrated supply chains, with many components crossing multiple borders before final assembly. Disruptions from tariffs increase production costs and reduce supply chain efficiency. Therefore, trade policy remains the central uncertainty for the sector. The Trump administration has re-imposed a baseline tariff of 10% on imports under Section 122 under the Trade Act following the Supreme Court’s ruling against IEEPA-based levies. We expect that the administration will seek to make those tariffs more permanent. At the same time, Washington declined to renew the USMCA trade pact, which will most likely move into rolling annual reviews. This trajectory will keep the agreement and its tariff exemptions in place for the time being, but it denies businesses the long-term certainty they need. This leaves the automotive sector exposed to weaker investment sentiment, softer cross-border capital flows and delayed expansion decisions across integrated North American supply chains.

For the US automotive industry all this reinforces long-running localisation trends, with higher import costs incentivising a gradual shift of production and component sourcing back to the US. Several domestic and foreign OEMs have started to relocate production, but higher labour and operating costs in the US are key concerns for businesses and discourage in particular the production of lower-margin vehicles. We expect that any sustained reshoring efforts are likely to be slow and uneven. Supply chain restructuring will remain a multi-year process, as manufacturers work to reshore production and diversify supplier networks.

In the EV segment the rollback of tax credits from October 2025 continues to weigh on demand. Large OEMs in the US have scaled back or even discontinued their original plans for EV production expansion. Currently EV production in the US is forecast to be 17% lower in 2030 than expected half a year ago. While internal combustion engine (ICE) production is still very high in the US, the recent trend over the past year or two is a rise in the popularity of hybrids.

US automotive production is expected to rebound by 3% in 2027, followed by 4.3% growth in 2028 as some major OEMs are expanding their capacity or opening new plants, or both. We expect to see increased vehicle prices for the time being.

After three years of annual contractions, the Canadian automotive sector is forecast to return to growth, with output expected to expand by 1.2% in 2026. However, the recovery is fragile and heavily dependent on the resolution of trade uncertainty as well as the successful restart of idled capacity by some major OEMs. In any case, the credit risk in the automotive suppliers' segment remains elevated.

Canada’s automotive industry is deeply integrated with US supply chains under the USMCA framework, with renegotiation beginning in early July 2026. While Canada has joined Mexico in supporting a 16-year extension of USMCA, the US has expressed its intention to not extend the agreement, preferring joint annual reviews over the next decade. This approach implies the persistence of current tariffs on both Canada and Mexico and potentially lengthy negotiation processes. Uncertainty would remain, weighing on investments in the industry. However, effective tariff rates applied to most of Canada's and Mexico's exports to the US will remain well below those imposed on the rest of the world, meaning that both will retain preferential access to the US market.

The medium-term production outlook rests heavily on the EV transition, but risks here are tilted to the downside. Honda Group has postponed a planned Alliston EV assembly plant and battery facility until at least 2029, reflecting the deterioration in EV demand conditions. A Chinese OEM foothold in Canada, made possible by the government’s decision to allow a 49,000-unit import quota at reduced tariff rates, could partially offset production losses over the longer term, but it does introduce new competitive dynamics for established players.

According to INEGI, Mexico´s statistics institute, automotive production decreased by 0.9% year-on-year in the January to May 2026 period, and we expect further decreases in the coming months. However, exports are still growing, particularly in the light vehicles segment. Higher US tariff levels on other trade partners and growing geopolitical tensions are likely to offer some benefit to the Mexican automotive industry, given its USMCA exemptions. Vehicles and parts from Canada and Mexico that are compliant with the USMCA trade agreement (where 75% of all parts in the finished vehicle must originate from the region) are only tariffed on their non-US content. Additionally, Mexico still benefits from a unique geographical advantage, and well-established interconnected supply chains.

However, the country’s reliance on the US market, which accounts for more than 75% of its auto exports, leaves the Mexican automotive industry highly exposed to trade uncertainty. The introduction of US import tariffs and regulatory barriers have raised production costs and lengthened supply timelines, leading to slower payments. Mexico supports a 16-year extension of USMCA but, as with Canada, the US has expressed its intention to not extend the agreement, preferring joint annual reviews over the next decade. This suggests the current tariffs are likely to continue and may include lengthy negotiation processes. Reports suggest the US is seeking to raise the minimum North America content for autos to 82% from 75% and set a 50% US content minimum. All this means that uncertainty remains, weighing on business confidence and capital investments in the Mexican automotive industry. OEMs and suppliers must continue to adjust their production strategies to cope with rising volatility.

Chinese automotive production growth is expected to slow down from 12.2% in 2025 to 1.9% in 2026. Domestic car sales are forecast to decline by 5.5% this year, as consumer sentiment remains subdued and higher fuel prices affect sales of ICE vehicles. However, China remains the principal engine of global automotive growth, underpinned by a reactivation of trade-in and scrappage subsidy schemes in March 2026 and by robust export volumes.

In the January to May 2026 period, passenger car exports reached 3.5 million units, up 69.6% year-on-year. Exports will remain robust in the coming months, due to structural cost advantages in EV production. Export diversification towards Southeast Asia, the Middle East and Latin America has helped to offset headwinds from EU tariffs on Chinese-built EVs. Higher global oil prices stemming from the Gulf conflict should accelerate EV adoption, providing an additional tailwind for car exports in the near term. However, broader protectionist trends are adding uncertainty to the export diversification strategy.

The Chinese automotive market continues its transition towards greater EV production, and EVs sales overtook ICE sales in the passenger car segment for the first time last year. The long-term prospects for EV production and sales growth are good, due to low vehicle densities and rising middle-class incomes in China. By 2030, EVs are projected to represent 65% of all new car sales in China, while ICE vehicles will decrease to 27%.

The booming EV market has attracted many new producers, which has led to overcapacities and fierce competition. A price war has been ongoing for three years, and average EV sales prices have decreased by about 20% in this period. In order to improve competitiveness or win a greater market share, both traditional and emerging players are being forced to step up R&D, launch new products, cut prices or launch limited-time promotions. Despite sales growth, this has led to dwindling margins.

Banks provide sizable credit facilities for traditional state-owned EV producers. However, many smaller private-owned businesses are not yet breaking even due to high input costs and are heavily reliant on external funding from investors. Without continuous capital flow, those firms could quickly fail. There have been several insolvencies over the past couple of years.

We expect a market consolidation in the medium term, in which the leading profitable producers prevail by adjusting their cost structures to accommodate permanently lower prices and by expanding their exports. Domestically, we expect competition to shift from a price-war dynamic towards technology and quality differentiation in the coming years. Autonomous driving, solid-state batteries, and premium EV positioning will become key battlegrounds among producers.

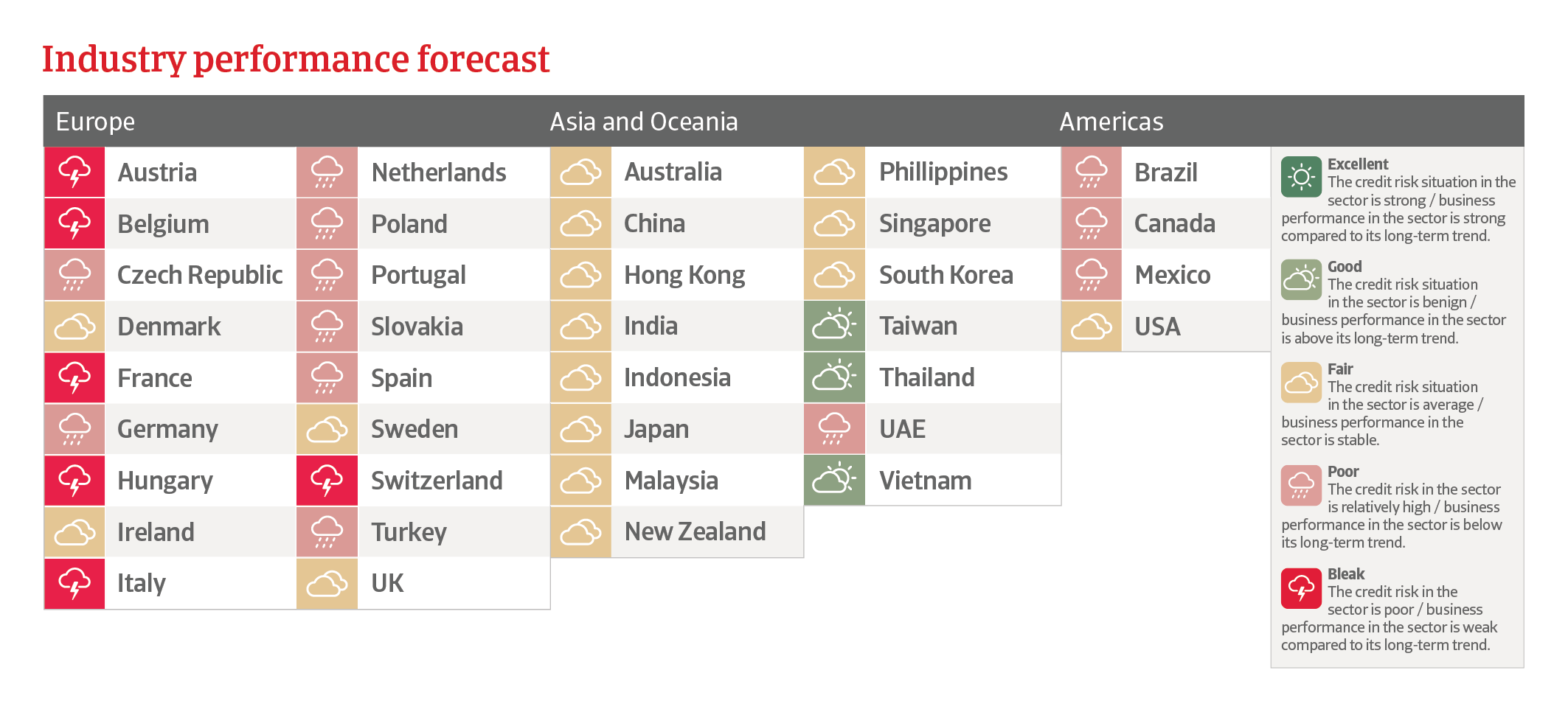

Suppliers are the most vulnerable segment, with less financial flexibility compared with OEMs. Suppliers suffer from late payments of up to six months, reinforced by the strong negotiating power of OEMs, which use price reductions to defend market share. The resulting margin pressure is increasingly being passed upstream, particularly small and medium-sized private suppliers with weaker bargaining power. Those are often required to accept both annual price cuts and extended payment terms, which weigh on their profitability, working capital and liquidity. In some cases, OEMs have stretched payment periods to more than 200 days, materially increasing receivable collection risk and cash flow pressure for suppliers. Credit risk for suppliers will remain elevated until price competition eases, overcapacity is addressed and payment discipline improves across the automotive supply chain.

We expect Japanese automotive production to contract by 3.6% in 2026 and by 2% in 2027. The situation in the main export markets is increasingly difficult. Shipments to Europe are decreasing as automotive demand in the region weakens, while Japanese brands face intensifying competition from domestic EV manufacturers in the Chinese market, eroding order books and factory utilisation. While US tariffs on Japanese auto exports have been lowered from 25% to 15%, this remains significantly higher than the previous rate of 2.5%. To address trade frictions with the US, major Japanese OEMs are planning to import US-built models in the domestic market, a move that will partially displace domestically produced volumes.

Restructuring is ongoing across several major OEMs, which continue to curb their domestic production bases and discontinue models as part of broader efforts to restore profitability. While Japanese OEMs retain a significant competitive advantage in hybrid technology, their slower rollout of EVs compared to Chinese and South Korean competitors raises concerns about longer-term export competitiveness. That said, the strength of Japan’s hybrid sector could benefit in the coming years in the US market, as the Trump administration has rolled back tax incentive schemes for EV sales.

Domestically, an ageing and shrinking population will weigh on sales in the coming years. The Japanese automotive sector’s medium-term outlook will depend on the success of new investment programmes targeting next-generation EV production and whether OEMs can reposition their export strategies in order to grow sales in emerging markets.

We expect South Korean automotive production to decrease by 7.6% in 2026 and by 3.5% in 2027. A combination of weak export momentum, domestic demand headwinds, and structural challenges weigh on the performance.

While US tariffs on South Korean auto exports have been lowered from 25% to 15%, this remains significantly elevated compared with a previous zero-tariff rate. South Korean car exports to the US amounted to USD 43 billion in 2024, accounting for about 6% of the country’s total exports. South Korean OEMs have invested heavily in EV technology and have established themselves as major exporters in this segment. Combined with the termination of EV tax credits in the US market, the import tariffs will slow the pace of EV exports and add to cost pressures in a sector already dealing with battery supply constraints and model-specific production volatility. However, in the medium term South Korea will remain a leader in high-tech automotive production, and large OEMs like Hyundai and Kia have a strong global market share, which can be built on.

Domestic automotive demand is expected to remain subdued, constrained by slower GDP growth, elevated household debt, and an ageing population. Car sales remain modest, rising by 0.7% in 2026, followed by a 0.1% decline next year. In the medium-term the South Korean car market will be increasingly characterised by replacement-driven demand rather than new household formation.

The ongoing expansion of overseas production capacity by Hyundai and Kia means that domestic production volumes will become increasingly decoupled from the commercial success of Korean brands globally, leaving the home production base more exposed to a structural decline in the long-term.

We forecast the automotive sector in the European Union to contract for a third year in a row in 2026, by 0.6%, before modestly recovering by 1.2% in 2027. Persistent affordability pressures, trade headwinds, and an uneven EV transition continue to weigh on production across the region. Production site overcapacities are a serious issue.

Demand conditions in the region remain subdued, as households’ real income gains are being offset by precautionary saving behaviour and a soft labour market in several member states. Consumer confidence remains low, which negatively affects big-ticket purchases like cars.

US import tariffs on EU-built vehicles are increasing costs for European OEMs with significant US export exposure and will accelerate production localisation in North America. At the same time, EU tariffs on Chinese-built EVs, ranging from 17.8% to 45.3%, offer only limited relief for European producers, given that Chinese manufacturers retain a substantial cost advantage. At least they provide European producers with a window to launch a new generation of more competitive vehicles. However, there is still the downside risk that China retaliates with export restrictions for rare earths and semiconductors.

Ongoing investment in EV platforms and battery supply chains remains a key driver of capital expenditure. However, transition-related uncertainty is complicating the business case for rapid electrification investment for manufacturers and suppliers alike. There is a need for clarity and planning certainty regarding the date on which ICE technology will be phased out. For manufacturers, the key question is how much longer they will need to invest in internal combustion engine technology rather than focusing entirely on electrification. Ongoing discussions and reconsiderations about the proposed phase-out of internal combustion engines from 2035 within the EU add to uncertainty in the industry. Any postponement would merely delay the associated problems.

We are observing shrinking margins and increasing payment delays and insolvencies in major markets. The shift away from internal combustion engines has started to reshape the industry and its competitive structure in Europe. Many Tier 2 and Tier 3 suppliers could lack the technological or financial means, or both, to climb up the value chain, and may be forced to leave the market in the coming years.

French automotive output is expected to grow modestly by 0.1% in 2026 and by 0.6% in 2027. This modest recovery will be fragile among structural challenges and global trade frictions. Volumes remain well below pre-Covid-19 levels, reflecting ongoing weaknesses in both demand and competitiveness.

Domestic demand conditions remain subdued, with car sales contracting 1.1% this year. This is due to subdued consumer confidence and lower purchasing power, ongoing political uncertainty, and a more demanding emissions-based taxation regime that is pushing up effective vehicle costs for middle-market buyers.

French manufacturers are relatively less exposed to US and Chinese trade tensions than their European peers, given limited direct exports to both markets. While the French automotive industry is relatively shielded from the impact of US tariffs, competitive pressure from Chinese EVs is rising. The ongoing transfer of production out of France, e.g. to Romania and Slovakia, will weaken domestic output. Capacity utilisation will remain below historical levels in the coming years, reflecting the structural shift away from high-volume domestic production.

Credit risk remains high for the whole sector, as profitability suffers from several factors: lower demand, rising costs for raw materials and logistics, investments in electrification, increasing regulatory pressure and fierce competition. Credit risk is highest among Tier 2 to Tier 4 suppliers. In this segment, low pricing, slowdown in demand, and tight operating margins have led to several defaults, from small to larger-sized businesses. We expect more insolvencies to come in the next 12 months. Major capital expenditure is required for shifting from internal combustion towards EVs. Many of those businesses that have already heavily invested in the electric transition now face subdued demand, resulting in financial strain.

The German automotive sector remains under pressure along the whole value chain. The industry is challenged by weak demand, shrinking margins, tariffs, and the shift away from internal combustion engines towards EVs, all at the same time. After contractions in 2024 and 2025, output is forecast to decline further, by 2.6% in 2026 and 1.8% in 2027.

For German OEMs both sales volumes and margins are decreasing, and pressure will mount in the coming years. Structurally, there is lower demand in Europe, while US tariffs on EU-built vehicles reduce German-sourced shipments to the American market. With the US serving as one of Germany’s most important export destinations, the 15% duties threaten to cut deeply into volumes and margins. Sales and market share in China are also decreasing, and the shift in consumer preferences toward domestic brands could accelerate this process, further reducing Chinese demand for German cars. Redirecting exports to other markets is, at best, a partial solution.

In order to stay competitive, German OEMs are undergoing substantial cost-cutting measures, including large job cuts. Although manufacturers are investing billions in electrification and software, and are doing their utmost to make up for lost ground, there is currently no sign of an upward trend.

Suppliers, in particular, are facing major challenges. The insolvency situation in this subsector remains tense, and the level of non-payments remains high. Banks are increasingly restrictive in providing loans to automotive suppliers. Therefore, it is more difficult for many businesses to obtain credit extensions or refinancing, which affects liquidity. In particular, smaller Tier 3 and Tier 4 suppliers are finding themselves increasingly under pressure because they lack the necessary financial buffers. Increasing competition is leading to a significant decline in sales. In addition, many companies are still focused on the manufacture of combustion engine components and are facing enormous conversion costs to secure their future.

In order not to lose the US market, several German OEMs are planning to set up production facilities in the US. Sooner or later, suppliers will have to follow suit and also relocate to the US in order to survive. However, many smaller suppliers will not be able to afford this. As a result, capacity in Germany will be reduced, in some cases irretrievably.

The scope for the defence industry to serve as a fallback for struggling automotive suppliers is limited. This is because the defence industry is uncharted territory for suppliers – with different structures, clients, business models and requirements. Defence programmes typically take years for suppliers to qualify, much longer than most automotive projects.

UK automotive production is forecast to return to growth in 2026, with output expected to expand by 3.5% following a sharp decline of 11.1% last year. This decrease was exacerbated by exceptional closures at Jaguar Land Rover in the second half of 2025. The underlying recovery is driven primarily by new EV-related production coming online, though the sector remains structurally fragile. Capacity utilisation is set to improve gradually from 43% in 2025 to around 51% by 2033 as plant closures reduce excess capacity, but this remains well below the 75%–80% level necessary for profitable operations.

Trade risks remain a significant structural constraint. Around 57% of UK automotive exports are destined for the EU, while close to half of components are sourced from the region, leaving the sector highly sensitive to any deterioration in UK-EU regulatory relations. Stricter rules-of-origin requirements, such as mandating that 45% of a BEV value must originate from the UK or EU, have been postponed to 2027. While this provides temporary relief, it creates a looming adjustment challenge for manufacturers. US tariffs on UK automotive exports have been cut to 10% (from 27.5% previously), 5 percentage points lower than US tariffs on EU exports under a significant 100,000 unit quota. This will give UK auto manufacturers some respite, but pressures on margins will remain.

Domestically, elevated oil and gas prices have raised inflation and squeezed household spending power, weighing on new car sales. We expect dealer margins to remain thin, with strong working capital management key if they are to successfully endure a more difficult car retail market.

Download the full report in the related documents section below for a detailed analysis of the challenges, performance, and credit risks facing the consumer durables/retail industry’s major markets throughout the world.

To explore to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Rückruf anfragen

Rechtlicher Hinweis