Atradius Atrium

Sie erhalten direkten Zugriff auf Ihre Vertragsinformationen, Tools zur Beantragung von Kreditlimits und Einblicke.

Österreich

Österreich

Australien

Australien

Belgien

Belgien

Brazil

Brazil

Bulgarien

Bulgarien

China

China

Dänemark

Dänemark

Deutschland

Deutschland

Finnland

Finnland

Frankreich

Frankreich

Griechenland

Griechenland

Hongkong

Hongkong

Indien

Indien

Irland

Irland

Italien

Italien

Japan

Japan

Kanada

Kanada

Litauen

Litauen

Mexiko

Mexiko

Neuseeland

Neuseeland

Niederlande

Niederlande

Norwegen

Österreich

Norwegen

Österreich

Polen

Polen

Portugal

Portugal

Rumänien

Rumänien

Schweden

Schweden

Schweiz

Schweiz

Singapur

Singapur

Slowakei

Slowakei

Slowenien

Slowenien

Spain

Spain

Tschechische Republik

Tschechische Republik

Türkei

Türkei

Ungarn

Ungarn

Vereinigte Arabische Emirate

Vereinigte Arabische Emirate

Vereinigtes Königreich

Vereinigtes Königreich

Vereinigte Staaten

Vereinigte Staaten

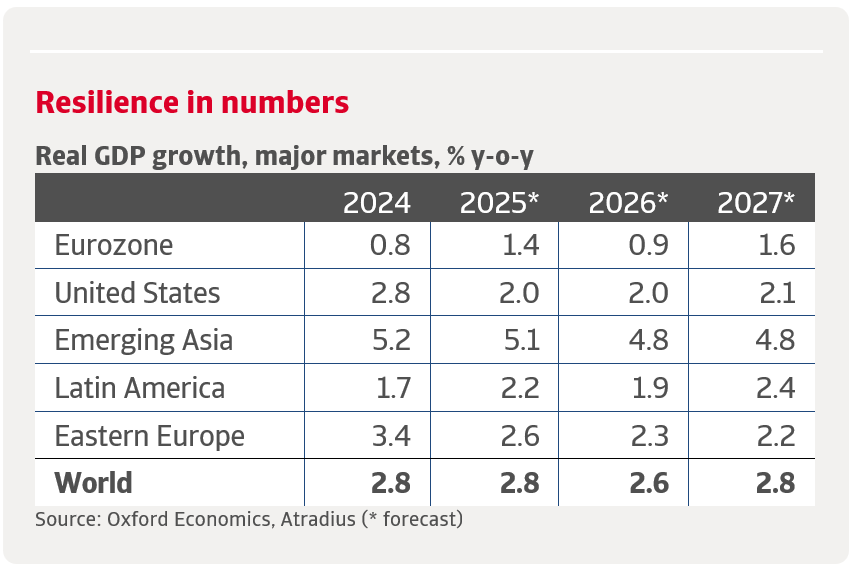

Global growth in 2025 has been surprisingly resilient, driven by an unprecedented boom in AI-related investment, particularly in the United States. Despite ongoing trade tensions and policy uncertainty, massive capital flows into AI infrastructure – data centres, chips, and power upgrades – have provided a significant boost to economic activity. This surge in AI investment is expected to continue, though at a slower pace, into 2026, masking some of the negative effects of the trade war and supporting global GDP growth.

Global GDP growth is forecast to moderate to 2.6% in 2026 and recover slightly to 2.8% in 2027. The US is expected to maintain growth around 2.0% in both years, while Emerging Asia remains the global growth leader, albeit at a somewhat lower rate. The eurozone is projected to see muted growth, at 0.9% in 2026 and a mild rebound to 1.6% in 2027. Latin America and Emerging Europe are forecast to hover around 2% growth.

Global trade growth, after a temporary lift in 2025, is expected to decelerate sharply. Trade grew by an estimated 3.5% in 2025, buoyed by frontloading and AI-related goods, but is forecast to stagnate in 2026 before recovering to around 2% in 2027. The trade war’s impact, though less intense than initially feared, continues to weigh on the outlook, with tariffs and uncertainty depressing trade volumes, especially between North America and Asia.

Advanced economies are set for subdued growth, with increasing divergence. The US economy is running on two tracks: robust AI-driven investment contrasts with weakening momentum in the broader real economy. The eurozone’s growth is supported by resilience in services and select countries like Spain, but the overall expansion remains modest due to weak consumer sentiment and investment.

Emerging market economies (EMEs) remain more resilient but face headwinds. EMEs are forecast to grow by 4.0% in 2026 and 4.1% in 2027, with India leading at over 6% growth. China’s growth is expected to slow below 5% as export momentum fades and structural challenges persist. Many EMEs benefit from integration into AI value chains, but are also exposed to US trade volatility, higher borrowing costs, and global financial uncertainty.

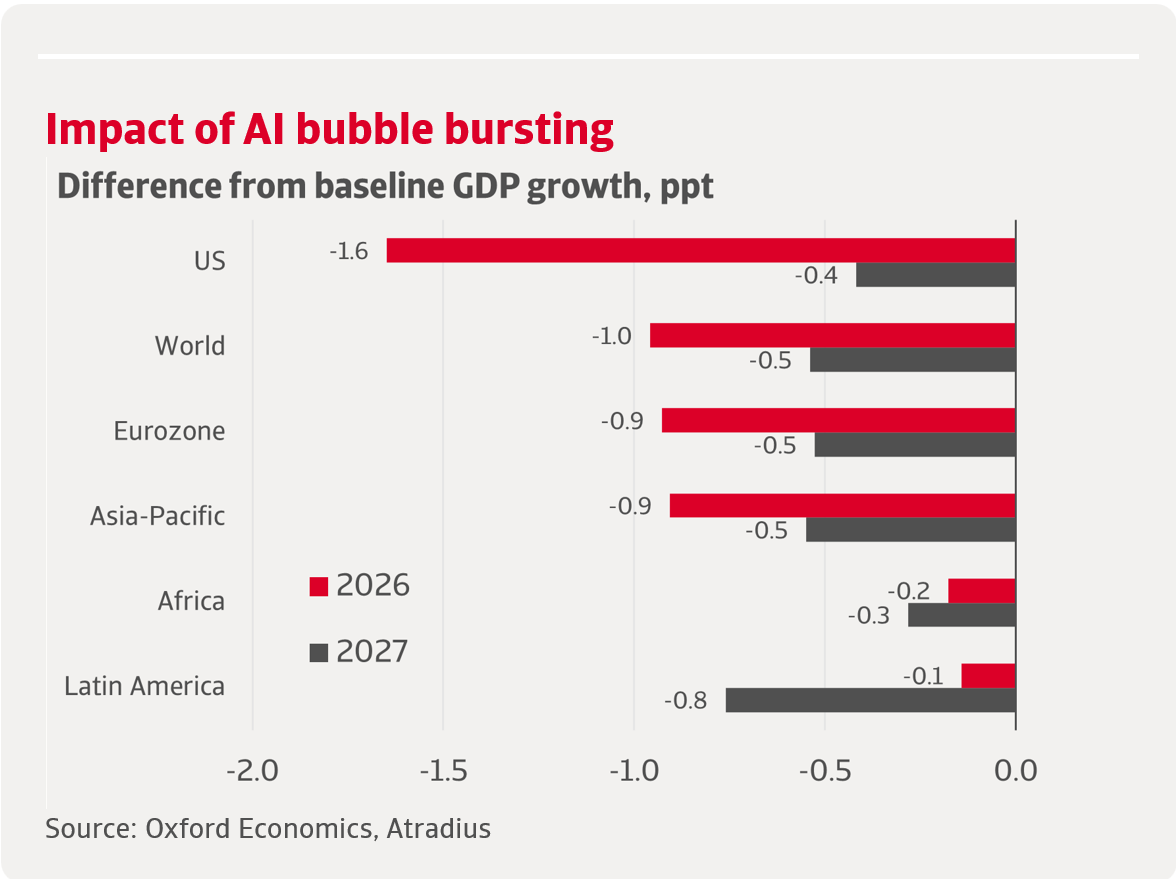

A sharp decline in confidence in the future benefits of AI could trigger an abrupt end to the current investment boom, resulting in a pronounced AI bubble burst. In this downside scenario, US tech stocks would fall by around 25%, leading to a significant loss of household wealth and a sharp slowdown in consumer spending and corporate investment, particularly in the technology sector. Exports would decline, business sentiment would deteriorate worldwide, and tighter financial conditions would amplify the shock. The US dollar would depreciate further, and the Federal Reserve would be forced to respond with additional rate cuts. This would lower global GDP growth in 2026 and 2027 by 1.4 percentage points. The impact would be most severe for the US and major tech exporters in Asia-Pacific, but spillovers would affect all regions.

For a complete overview of the impacts and risks of the rise in AI, ongoing trade war and more on our global economic outlook, download the full report available in the related documents section below.

Rückruf anfragen

Rechtlicher Hinweis