Amsterdam 25 January 2022 – The strong rebound in GDP across most of the world may prove to be more of a bounce than a movement.

Purchasing power, bolstered in many cases by government intervention was strong in 2021. Despite strong product demand, supply chain issues have left factory shelves depleted and driven inflation sky high. In the US, the inflation rate hit 4.6%, the highest of the developed markets, and is expected to remain relatively high at 4.0% in 2022. Eurozone inflation hit 2.5% and is forecast to remain close to this level at 2.3% in 2022. This could dampen demand in 2022 and 2023 leading to slowing growth rates and rising insolvencies.

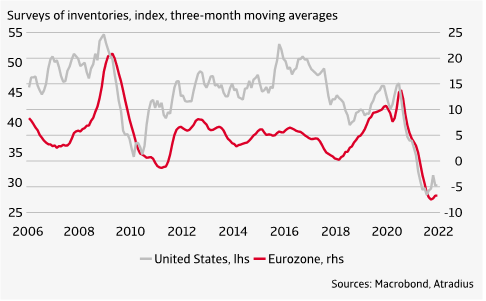

Inventory indexes at historical lows

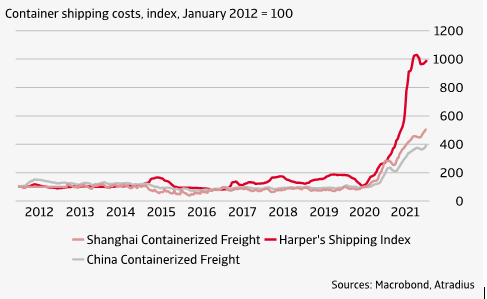

With new more contagious covid-19 variants driving infection rates to record highs the visual impact of the pandemic is readily evident with new lockdowns resulting in lower traffic levels, closed stores and hospitality businesses, less travel, still understaffed offices and less crowded downtown areas. Despite this, demand for consumer durables products in particular has been good. Getting these goods to market however has been an issue. The pandemic has triggered a number of supply chain bottlenecks that have delayed shipment of raw materials and finished products, depleted stock levels, and driven up freight costs. With these factors driving prices higher and skyrocketing fuel prices due to OPEC production caps and gas shortages, despite the surge in demand, slower GDP growth is anticipated in 2022 and 2023.

Record high shipping costs

Although the spike in inflation is eroding purchasing power, we expect global GDP growth to slow, but remain positive. Despite the rising inflation, consumer savings have accumulated and, to a modest extent, should offset inflation. Supply chain disruptions should abate in the second half of 2022 and in 2023. This, along with monetary policy mainly in advanced markets, should create some inflation relief.

Our current take on the situation is that current levels of inflation are temporary and will not persist. Inflation pressures will largely fade in the next two years as the current phase reflects an abnormal situation. Wage pressures are still relatively low and inflation expectations remain well anchored. We do see that high inflation is gradually forcing central banks to start monetary tightening, but more so in the US than in the eurozone.