In France, the number of insolvencies is forecast to increase 3% this year due to decelerating economic activity.

The outlook is more optimistic regarding household spending as consumer confidence keeps rising. Although investment is set to cool down, it should remain more dynamic than economic activity in general. In 2020, insolvencies are expected to level off.

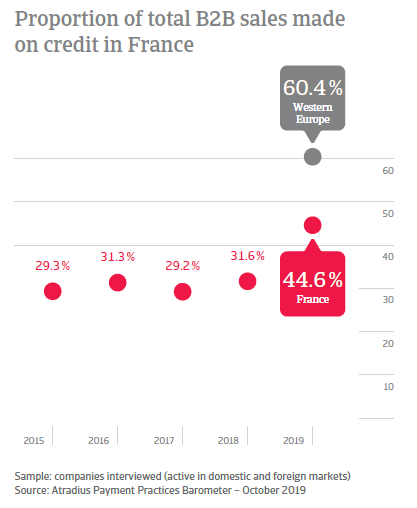

Perception of payment default risks arising from selling on credit appears to be strongest in France than elsewhere in Western Europe

Survey findings in France show suppliers sold 44.6% of sales to B2B customers on credit (up from 31.6% last year). This is the lowest proportion of credit-based sales recorded across all the countries surveyed in Western Europe and is notably below the 60.4% regional average (up from 41.4% last year). Although survey respondents in France appear to have granted credit terms to their B2B customers more often than one year ago, the percentage of their credit-based sales is the lowest in Western Europe. Suppliers surveyed in France appear to have the most prudent approach in the region to trading on credit in challenging economic times, and a strong aversion to the risk of payment default arising from selling goods and services with deferred payment.

The trade credit policies of French respondents is as strict as last year

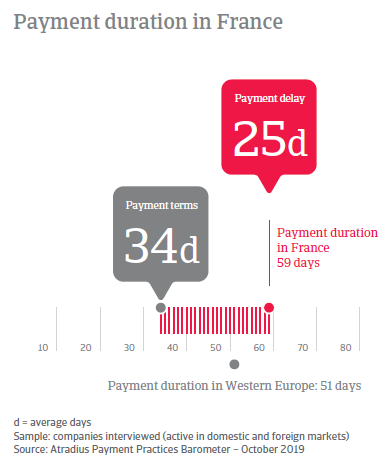

Suppliers surveyed in France appear reluctant to give B2B customers longer to settle invoices than last year. Uncertainties regarding trade policy developments worldwide weigh heavily on economic activity and increase financial risks significantly. This may explain why average payment terms recorded in France stand at 34 days from invoicing (compared to 33 days last year). These are in line with the 34 days average for Western Europe.

Unlike their Western European peers, suppliers surveyed in France reserve against bad debts more often than sending dunning letters

The most popular credit management techniques employed by suppliers surveyed in France include assessments of creditworthiness and reserving against bad debts. Credit assessments are performed prior to trade credit decisions by 31% of survey respondents (compared to 35% in Western Europe). The creation of a bad debt fund is also performed by 31% of French businesses (24% in Western Europe) and is often used to offset any potentially inaccuracies in the screening of the buyer’s financial position. Such widespread use of these credit management techniques is likely to be a reflection of heightened perceptions of the payment default risk arising from selling on credit in challenging economic times. Interestingly, far more French respondents (nearly 30%) than in Western Europe (22%) reported they requested B2B customers to pay invoices in cash or on terms other than trade credit over the past year. This further corroborates evidence of the strong aversion of French suppliers to the risk of payment default arising from selling goods and services with deferred payment. A standout survey finding is 22% of French respondents (above the 16% at regional level) have opted for self-insurance over the past year.

Far more respondents in France than in Western Europe reported their business to be significantly impacted by late payments

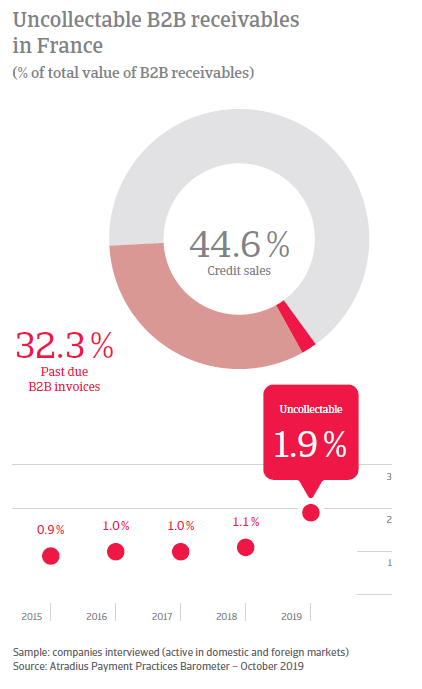

32.3% of the total value of the B2B invoices issued by survey respondents in France over the past year remained outstanding at the due date. This is above the 29% regional average. Consistent with improved payment habits from their B2B customers, resulting in increased timely payments (63.4% of invoices paid on time compared to 55.9% last year), respondents in France were able to turn overdue invoices into cash on average three days earlier than one year ago (59 days down from 62 days last year). This variation is consistent with observations for the region overall, where the invoice-to-cash turnaround decreased on average to 51 days down from 57 days last year. Despite their heightened perception of payment default risks, and their consequent prudent approach to trading on credit, far more respondents in France (81%) than in Western Europe (58%) reported their business was significantly impacted by late payments. To protect the business from untimely payment of invoices, far more respondents in France (36%) than in Western Europe (26%) needed to take corrective measures to safeguard cash flow. Similarly, far more respondents in France (32%) than in Western Europe (20%) needed to pursue additional financing from banking and factoring. In terms of collection of long-term past due invoices, suppliers surveyed in France appear to be less efficient than one year ago. Survey findings show that the proportion of write-offs of uncollectable accounts increased to 1.9% (up from 1.1%) over the past year. However, this is below the 2.2% average for Western Europe.

Almost a third of businesses in France expect their customers’ payment practices to deteriorate over the coming months

Far fewer survey respondents in France (45%) than in Western Europe (55%) believe that, over the coming months, the payment practices of their B2B customers’ will remain reasonably consistent with the current practices. 30% of French survey respondents (above the 25% at regional level) expect payment practices to deteriorate over the same time frame. Specifically, the expected deterioration is forecast to result in an increase in long-term overdue invoices (over 90 days past due). To improve protection of business profitability against the risk of insolvency from customers, far more respondents in France (37%) than in Western Europe (28%) plan to request cash payments from B2B customers. 35% of respondents will increase the performance of checks of their customers’ credit quality and will send dunning letters. This is in line with what was reported by respondents in Western Europe. Far more respondents in France (36%) than in Western Europe (25%) express concern about access to bank financing and fear this will become more troublesome over the coming months. On average, 36% of respondents in France will seek to balance capital costs by cutting operational expenses.

Overview of payment practices in France

By business sector

B2B customers in the French chemicals sector are given the longest to settle invoices: the consumers durables sector has the shortest payment terms

Based on survey findings in France, the longest payment terms are seen in the chemicals sector (terms average 69 days from invoicing). Average payment terms across the other sectors surveyed in France range from 48 days in the machines sector to 27 days in the agri-food sector. At the lower end of the scale, is an average of 26 days granted by respondents in the consumer durables sector.

Trade credit risk worsened markedly in the French chemicals sector over the past year

Despite being given the most relaxed credit terms, payment practices of B2B customers in the French chemicals sector deteriorated markedly over the past year. However, it is the machines sector in France that records the highest proportion of past due payments (43% of the total value of invoices issued in the sector remained unpaid at the due date). Across the other sectors surveyed in the country, the average percentage of overdue invoices ranges from an average of 33% in the construction and consumer durables sectors to 27% in the transport sector. The lowest proportion of overdue B2B invoices was recorded in the agri-food sector.

Chemicals sector markedly less efficient in collecting long-term overdue invoices than one year ago

Consistent with the marked deterioration of trade credit risk in the French chemicals sector, the proportion of long-term overdue B2B receivables written off as uncollectable increased significantly over the past year (to 2.4% from 1.3% one year ago). Over the same period, the collection of overdue receivables in the agri-food sector improved, with a corresponding decrease of write-offs to 1.6% of B2B sales on credit from 1.8 last year. The ICT/electronics sector in France records the lowest proportion of receivables written off as uncollectable (1.4%).

By business size

French large enterprises granted the longest average payment terms

Respondents from large enterprises in France extended the longest payment terms to B2B customers, averaging 57 days from invoicing. Micro enterprises offered average payment timings at 24 days, and SMEs at 33 days.

Large enterprises are the slowest to cash in past due payments

Large enterprises are the slowest in collecting past due payments, with an invoice-to-cash turnaround at 86 days from invoicing (down from 41 days one year ago). Payment practices of B2B customers of French SMEs improved notably over the past year. The proportion of timely paid invoices registered an average 8% increase compared to one year ago. Due to this improvement, French SMEs are now able to collect past due invoices far earlier than last year (on average within 59 days from invoicing down from 66 last year). The time it takes French micro-enterprises to cash in past due payments averages 43 days from invoicing (stable compared to last year).

French SMEs markedly less efficient in collecting long term overdue receivables than last year

Despite the improved payment practices of their B2B customers, French SMEs record the highest proportion of long-term overdue invoices written off as uncollectable (2.2% up from 1.3% last year). The same thing can be said about large enterprises, where the portion of write offs increased to 1.8% from 1.1% last year. Micro enterprises record an average of receivables written off as uncollectable at 1.1% (up from less than 1% one year ago).

Yves Pierre Poinsot, Atradius Country Manager for France commented on the report: “The French economy is expected to grow at an average annual rate of 1.3% this year, mainly driven by a resilient domestic demand. In contrast, the uncertain international environment is forecast to weigh on the country’s economic activity, particularly due to the difficulties that Germany’s economy is facing and the tight financial conditions in Italy.

Escalating trade tensions, along with the uncertainties over the outcome of Brexit keep on posing downside risks to the current outlook. These factors threaten the financial stability of businesses, thus triggering an expected increase in insolvencies.

Survey findings in France reveal that businesses have a prudent approach to the use of trade credit in B2B transactions, as they have a strong perception of the payment default risk that arises from selling with deferred payment. Many businesses report to have been hit hard by late payments and many are pessimistic about the future. Therefore, the economic climate becomes more uncertain and volatile, a solid assessment of the credit quality of the customers and a strategic management of trade receivables is essential to safeguard cash flow and avoid severe liquidity issues, enabling the business to grow safely despite challenging economic times.”